office (412)

967-9367

office (412)

967-93673.6

Two-Period European versus American Option Example

|

I |

n

this topic, we start by working through a two-period European option pricing

problem, and then compare it with American options.

We use the risk-neutral valuation principle since it provides a

straightforward method for computing the values for both types of options.

Assume

the following:

S = $10

u = 2

d = .5

r = 1.01 per

month

X = 15

1-period

= 1 month

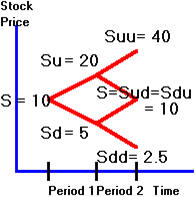

Here,

the initial stock price of 10 can double or halve every period.

Using the tree representation, we get the results shown in Figure 3.7.

Figure 3.7

Tree Representation for Stock

European

option values defined on this tree can be computed in a straightforward manner

by using the risk-neutral probabilities. Recall

that these probabilities are:

respectively,

for an uptick and a downtick. In

this example, these equal 0.34, and 0.66, respectively.

European

Call Option Values

The

value of a European call option at the uptick node is obtained from the formula:

where

Cuu and Cud

are the terminal values of the call option (i.e., the values of the call at the

two nodes after the first uptick). A

similar procedure is applied at the downtick node, and finally repeated at the

initial node. The call option tree is depicted in Figure 3.8.

Figure 3.8

Tree Representation for Call Option

Here,

Cuu = 25 = Suu

- X = 40 - 15.

American

Call Option Values

You

have seen (topic 3.3, American Call Option: Zero-Dividend Case) that if there are no dividends, a

call option should not be exercised early.

Since the stock in this example does not pay any dividends, this means

that the American option should be worth exactly the same as the European one.

You

can verify this using this same example. In

the tree, shown in Figure 3.9, there are two values depicted at each node. The bottom value is what you get if you exercise the call,

and the top value is what you get if you do not exercise the call.

Figure 3.9

Call Value: Exercised versus

Unexercised

Clearly,

you would not choose to exercise at any node, except where there are two upticks.

European

Put Option Value

You

can compute the European put values, strike = 15, at each node either from the

risk-neutral valuation principle or from put-call parity.

The tree diagram for put values is shown in Figure 3.10.

Figure 3.10

European Put Option Values

American

Put Option Value

Recall

(see topic 3.4, American Put Option: Zero-Dividend Case) that even without dividends, there

may be value in early exercise of an American put option.

As a result, you have to check for this possibility at every node.

The

tree in Figure 3.11 displays two values at each middle node and three values at

the first node. The top number is

the (European) value of the unexercised put option, and the bottom

(middle) number is the value of the put option exercised.

The bottom number at the first node is the American put value and online

it appears in red:

Figure 3.11

American Put Option Value

You

can see that if a downtick occurs in period 1, the stock price equals 5 and the

exercised value of the put option is 15 - 5 = 10.

The unexercised value is the

same as the European put option value of 9.85.

As a result, the risk-neutral price at time 0 is now:

In

the next topic Two-Period Asian Option Example

you can see how to apply the binomial model to the problem of valuing a non-standard

option.